Rising Complexity Becomes Defining Challenge inVehicle Logistics, INFORM Study Finds

Apr 8, 2026

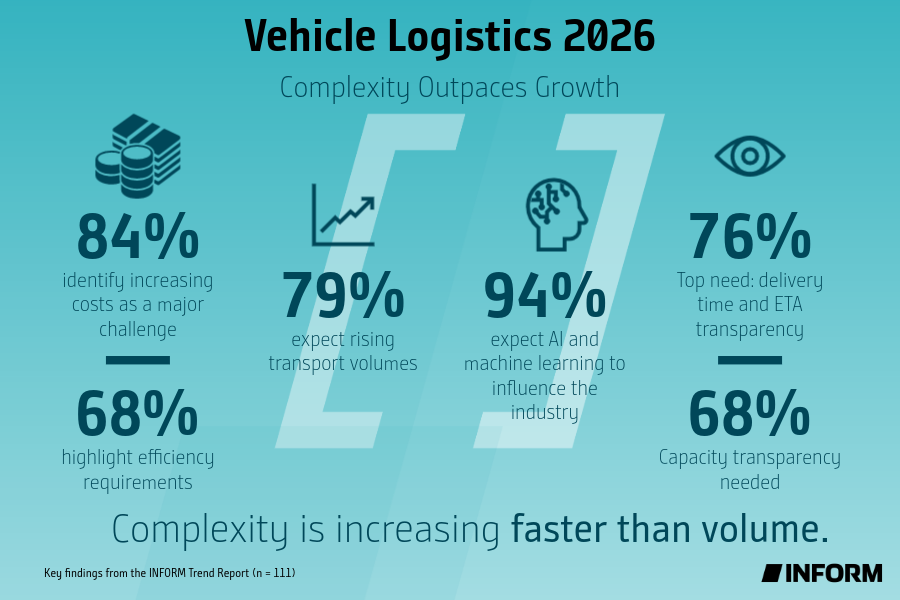

Vehicle logistics is entering a new phase defined less by growth alone and more by the challenge of managing increasing operational complexity. This is the central finding of the INFORM Trend Report 2026: IT in Vehicle Logistics, based on a survey of 111 industry professionals.

While 79% of respondents expect vehicle transport volumes (rather than overall production volumes) to increase over the next five years, a large majority simultaneously report continuously rising operational pressure. 84% identify increasing costs as the dominant challenge, followed by growing efficiency requirements (68%) and fluctuating volumes (52%).

Cost pressure remains the dominant operational challenge and has intensified compared to previous surveys (2013, 2018, 2023). At the same time, limited transparency and increasing network complexity continue to impact planning quality and execution reliability. In many organizations, fragmented information still leads to reactive rather than proactive decision-making.

Management Summary: Growth Continues – Complexity Accelerates

The study highlights a structural shift in vehicle logistics:

- Most respondents expect transport volumes to grow.

- Operational pressure is intensifying across networks.

- Complexity is increasing faster than volume.

As a result, vehicle logistics is evolving into a decision-making challenge under cost and coordination constraints. Limited transparency remains a key barrier to efficient operations:

- 76% report insufficient visibility of delivery times and ETA.

- 68% see gaps in capacity transparency.

- 66% highlight missing transport status visibility.

At the same time, companies see a growing gap between operational requirements and existing IT capabilities. While 95% expect IT systems to improve operational efficiency, many organizations still struggle with fragmented data, limited integration, and insufficient decision support.

From Visibility to Decision Intelligence

Vehicle logistics networks involve multiple independent actors — from OEMs to carriers, terminals, ports, and dealers — each operating with their own systems and planning processes. As networks grow more interconnected, coordination becomes significantly more complex. Thus, the results indicate a clear shift in priorities: “Transparency alone is not the final objective. The real challenge is turning operational data into better decisions across the logistics network,” said Dennis Feddern, Senior Vice President Vehicle Logistics at INFORM.

Artificial Intelligence (AI) is widely expected to play a key role in addressing these challenges. 94% of respondents believe AI and machine learning will significantly impact the industry. It is expected to support the evaluation of complex scenarios and improve decision-making, with its primary role seen in augmenting human expertise rather than replacing it. However, the study also shows that immediate priorities remain more fundamental: better system integration, real-time visibility, and flexible planning capabilities.

A Long-Term Structural Trend

The INFORM study series (2013–2026) reveals a consistent pattern: vehicle transport volumes are expected to grow, while operational environments become more complex and volatile. Hartmut Haubrich, also Senior Vice President Vehicle Logistics at INFORM, added: “While many companies still expect growth, what we currently observe in the market is a more differentiated picture across regions. Regardless of short-term developments, the need to improve planning capabilities and decision-making remains unchanged.”

The study is based on a survey conducted between December 2025 and January 2026, with 111 professionals and managers from the global vehicle logistics industry. Participants include representatives from: automotive manufacturers (37%), logistics service providers (46%), as well as carriers, terminal operators, and port authorities.

The majority of respondents are based in Europe (62%), followed by North America (18%), with additional participants from South America, Asia, and Africa. Most participating companies operate in finished vehicle logistics, with 98% handling new vehicles, 50% handling used vehicles, and 30% involved in high and heavy transport. The survey was conducted anonymously using a structured online questionnaire consisting of 25 questions.

More information and the full survey results can be found here.